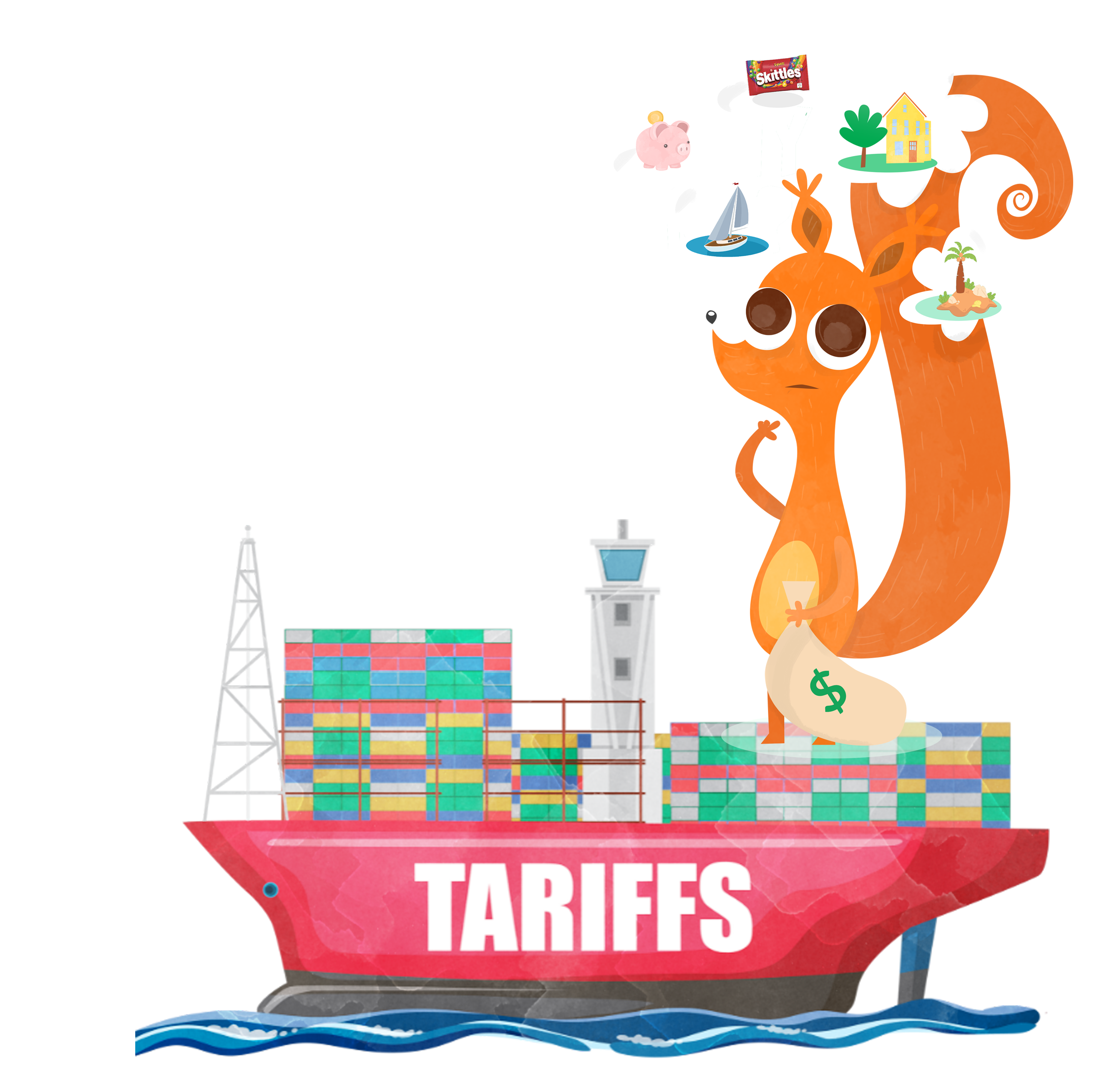

When you hear the word tariffs, your brain might immediately go to politicians arguing on TV, international trade deals, or giant shipping containers coming into port. But while all that might feel a world away, tariffs can have a real impact on your everyday life, especially your finances.

From groceries and gas to home upgrades and retirement accounts, tariffs can quietly raise costs and shake up your financial plan without you even realizing it.

So, what exactly are tariffs, how do they show up in your daily life, and what can you do about them? Let’s break it all down.

In simple terms, a tariff is a tax that a country charges on goods brought in from another country. So if the U.S. places a tariff on furniture imported from Vietnam, that furniture becomes more expensive for U.S. companies to buy.

But here’s the key: businesses almost never eat that cost themselves. Instead, they raise prices to make up for it. Eventually, that cost lands in your shopping cart, your home renovation quote, or even the price you pay for everyday services.

Even though you won’t see the word “tariff” printed on your receipt, their effect can sneak into your spending in a bunch of ways. Here are a few places you might notice changes:

If tariffs are placed on imported food items or ingredients, it increases the cost of bringing those goods into the country. That price hike works its way through the supply chain and eventually hits the shelf. Items like coffee, chocolate, canned goods, and fresh produce can become noticeably more expensive—especially if they rely on packaging or ingredients from abroad.

Building or upgrading your home might cost more than you expect if materials like lumber, tile, or steel are affected by tariffs. Even if you’re just hiring someone to redo your deck or replace your windows, the increased material costs will often be built into the contractor’s quote. This can be frustrating if you’ve already budgeted and suddenly find out you’re coming up short.

Lots of electronics and appliances rely on components made overseas. When those parts are hit with tariffs, the cost of assembling and selling the finished product goes up. That might mean you end up paying more for a new laptop, TV, refrigerator, or even small things like headphones and phone chargers.

Tariffs can disrupt global supply chains, especially in the energy sector. If importing oil becomes more expensive, fuel prices at the pump can rise. That means everything from your daily commute to your summer road trip could cost more. And if airlines face higher costs for imported parts or fuel, ticket prices can increase too.

The ripple effect of tariffs isn’t just about what you spend—it can also impact what you earn through investments. Here’s how that can play out:

Tariffs often create uncertainty in the markets. When companies don’t know what their costs will be, or if they’ll be able to keep selling to foreign buyers, stock prices can swing up and down. That kind of unpredictability can be stressful for investors, especially those nearing retirement.

Big companies that rely heavily on international trade can take a hit when tariffs are imposed. If profits fall, their stock prices might follow. If your portfolio includes global brands in sectors like tech, manufacturing, or retail, you might see some movement based on how they’re affected by trade policies.

When tariffs push prices up across the board, it contributes to inflation. That means the money you’ve saved—especially in low-interest accounts—doesn’t stretch as far. If inflation rises faster than your investment returns, your purchasing power quietly shrinks over time.

You can’t control global trade policy, but you can make smart decisions to protect your finances from unexpected shifts. Here are some simple but effective steps you can take:

If you’re noticing higher costs at the grocery store or gas pump, go back to your budget and see what can be adjusted. Maybe it’s time to pause a few subscriptions you’re not using, cook at home more often, or swap a few brand-name items for lower-cost alternatives. The goal isn’t to cut everything—it’s to be more intentional about where your money is going.

Tariffs can raise the price of certain imported goods, but there are often workarounds. Local products might be more affordable and just as high-quality. Compare prices, use apps to find deals, and consider buying secondhand when it makes sense. The more flexible you are with your choices, the better you can avoid inflated prices.

When prices are rising and the economy feels shaky, having a financial cushion becomes even more important. Aim to set aside three to six months of living expenses if possible. It gives you breathing room in case of job changes, unexpected bills, or just to help you feel more stable when everything else feels uncertain.

If market headlines are making you nervous, it might be time to take a fresh look at your investment strategy. Are you too heavily invested in sectors affected by global trade? Are your risk levels aligned with your timeline and comfort zone? It’s worth checking in to make sure your investments are still a good fit for your goals.

Tariffs might sound like something that only affects big companies and global politics, but they can quietly shape your everyday spending, the cost of big purchases, and even your retirement savings.

The good news is, a little awareness goes a long way. By keeping an eye on where your money is going and making small adjustments, you can stay in control—even when the global economy throws a few surprises your way.

And if you’re not sure where to begin, a free financial plan can help you figure out where you stand and what’s worth focusing on first. Think of it like a financial check-up that gives you a clear picture and a path forward.

YOUR FREE FINANCIAL PLAN

Are you ready to invest in your future?

Build your free plan today.

Start now

You do not need to become a “finance person” to improve your finances. You do not need to memorize stock terminology, optimize every purchase, or start speaking in mysterious podcast phrases about passive income streams while holding a steel water bottle. You mostly need: clearer systems less fear slightly better habits enough understanding to make calmer decisions

Low housing prices. Lower taxes. Lower monthly costs. A slower pace of life. Maybe a suspiciously affordable lakeside condo smiling at you from a real estate listing like a trap in a fairy tale. And to be fair, affordability matters. A lot.

Track every category. Review every receipt. Color-code your life. Become the kind of person who enjoys looking at bank statements on a Sunday. For most people, that version does not stick. Not because they are bad with money. Because the setup is too fussy, too time-consuming, or too annoying to survive real life. A beginner budget does not need to be perfect. It needs to be usable.